Economic output fell at its fastest pace on record last spring as the coronavirus pandemic forced businesses across the United States to close their doors and kept millions of Americans shut in their homes for weeks.

Business ground to a halt during the pandemic lockdown in the spring of this year, and America plunged into its first recession in 11 years, putting an end to the longest economic expansion in US history and wiping out five years of economic gains in just a few months.

A recession is commonly defined as two consecutive quarters of declining gross domestic product — the broadest measure of the economy.

Between January and March, GDP declined by an annualized rate of 5%.

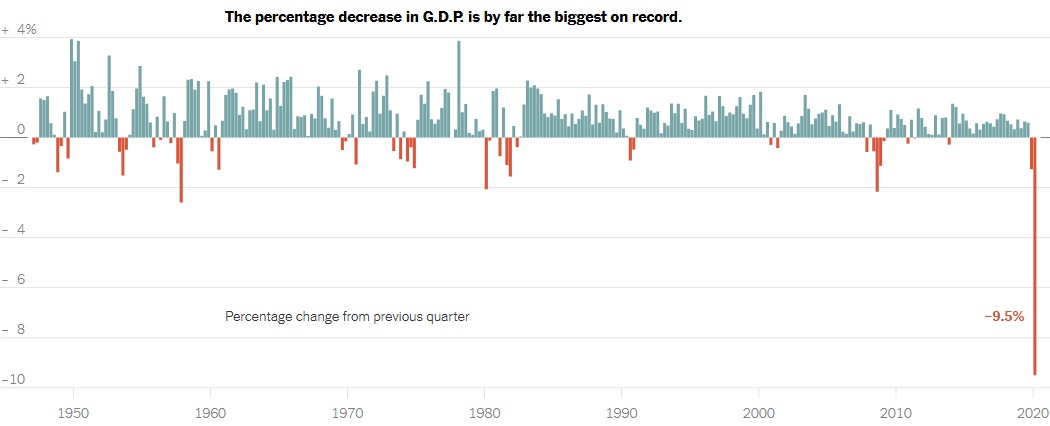

Gross domestic product — the broadest measure of goods and services produced — fell 9.5 percent in the second quarter of the year, the Commerce Department said today.

On an annualized basis, the standard way of reporting quarterly economic data, G.D.P. fell at a rate of 32.9 percent.

The collapse was unprecedented in its speed and breathtaking in its severity.

The only possible comparisons in modern American history came during the Great Depression and the demobilization after World War II, both of which occurred before the advent of modern economic statistics.

Unlike past recessions, this one was a result of a conscious decision to suspend economic activity to slow the spread of the virus.

Congress pumped trillions of dollars into the economy to sustain households and businesses, limit long-term damage and allow for a rapid rebound.

The plan worked at first. In recent weeks, however, cases have surged in much of the country.

Data from public and private sources indicate a pullback in economic activity, reflecting consumer unease and renewed shutdowns.

“In another world, a sharp drop in activity would have been just a good, necessary blip while we addressed the virus,” said Heather Boushey, president of the Washington Center for Equitable Growth, a progressive think tank. “From where we sit in July, we know that this wasn’t just a short-term blip.”

But this is no ordinary recession.

The combination of public health and economic crises is unprecedented, and numbers cannot fully convey the hardships millions of Americans are facing.

In April, more than 20 million American jobs vanished as businesses closed and most of the country was under stay-at-home orders.

It was the biggest drop in jobs since record-keeping began more than 80 years ago. Claims for unemployment benefits skyrocketed and have still not recovered to pre-pandemic levels.

While the labor market has been rebounding since states began to reopen, bringing millions back to work, the country is still down nearly 15 million jobs since February.

Next week’s July jobs report is expected to show another 2.3 million jobs added.

That would bring the unemployment rate down to 10.3% — still higher than during the worst period of the financial crisis.