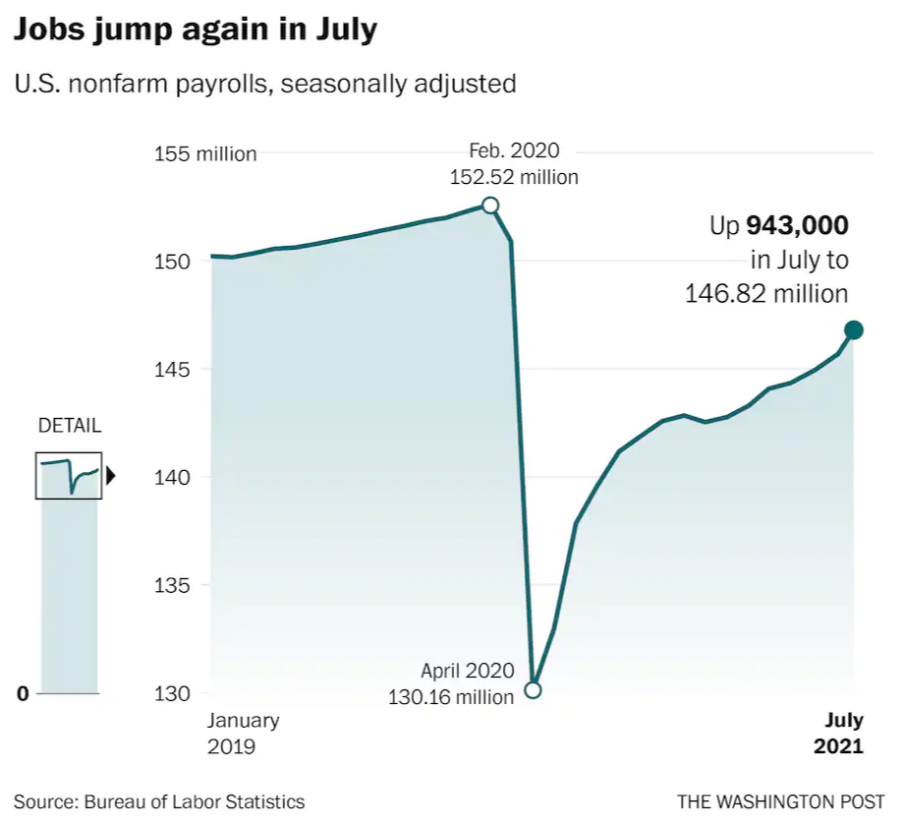

The U.S. economy added 943,000 jobs in July as hiring surged and employers raised wages to lure workers.

It marked the second straight month of impressive growth as the country’s recovery sped up amid widespread availability of vaccines.

But the renewed strength of the coronavirus in late July and early August is raising concerns about whether this momentum can continue.

The delta variant has sped through the country’s vaccine-resistant population in recent weeks, leading to new government restrictions.

That has clouded many economists’ outlook for the second half of the year and raised questions about whether July could serve as a high-water mark of the recovery’s second wave.

The unemployment rate in July fell to 5.4 percent from 5.9 percent, a sizable monthly reduction.

It is down from 6.3 percent when President Biden took office but still well above the 3.5 percent rate in February 2020, the final report before the pandemic slammed into the United States and sent joblessness numbers spiking to historic levels.

July’s tally was the highest number of jobs added since last August, and it surpassed June’s impressive numbers, which were revised up in the report to 938,000.

Economists, political leaders, executives and many workers are now watching to see where the economy goes from here.

In the weeks since the hiring data was collected, numerous firms began requiring vaccinations or imposing new mask restrictions on employees, as rising cases have begun prompting many companies to delay office reopenings.

The stock market, though, remains at record levels, and the recent reports about brisk hiring in June and July show that this momentum could be hard to knock off course.

June and July make for two straight months when nearly 1 million jobs were added — totals that are close to the optimistic predictions many economists had last year about how vaccinations would smooth the way for the labor market recovery.

And there were other promising signs in the report. Wages also continued to rise, raising by 11 cents an hour to $30.54 on average — the fourth straight month of growth.

The number of people reporting both long-term unemployment and temporary layoffs fell precipitously.

“This is an unambiguously positive report,” said Mark M. Zandi, chief economist of Moody’s Analytics. “It’s consistent with a booming economy, an economy that’s roaring back from the pandemic recession.”

Joe Brusuelas, chief economist at the firm RSM, agreed that the report showed exceedingly strong momentum.

“I’ve been doing this a long time — this is one of the best monthly jobs reports that I’ve seen in my career arc,” he said.

Biden touted the numbers at a morning appearance where he talked about the importance of his infrastructure plan, saying that more than 4 million jobs have been added since he took office.

“What is indisputable now is this: The Biden plan is working, the Biden plan produces results and the Biden plan is moving the county forward,” he said.

If there was a caveat about the report, it was its timing. The report is a portrait of the economy from the middle of July — around the beginning of the time when coronavirus cases from the delta variant began to surge.

The country is in a unique place, having confronted a number of conflicting forces in 2021 as the economy works to dig out of a public health crisis unlike any other in the modern era.

While vaccinations have given the country its strongest tool yet in the battle against the virus, the crisis is far from over, as resistance to the vaccine and the potential for the virus to continue to mutate make it hard to forecast how the intertwined crises — an economic one on one hand, and the public health one on the other — will unfold next.

There has been a notable uptick in inflation, though experts are split over whether it will be short-term or more lasting.

Employers continue to complain about labor scarcities, particularly for low-wage jobs, though there is some evidence that it can be partially addressed through things like better pay and benefits, as well as the wider availability of in-person schooling that is expected in the fall.

Hiring slowed in the winter as the virus raged, but it has picked up with sustained velocity in recent months.

The biggest jump has come in the leisure and hospitality sector, as hotels and restaurants worked to bring employees back, optimistic about a consumer spending boom.

These types of businesses, though, are susceptible to a setback if the virus doesn’t ebb this fall, making some of these gains fleeting.

Economists like Constance Hunter, chief economist for accounting firm KPMG, said it was too soon to tell how severely the latest surge of coronavirus cases, which is threatening the country’s reopening, will affect the labor market, but said there were reasons to be concerned.

The economy remains about 5.7 million jobs down from where it was before the pandemic hit in March 2020, and economists have expected the jobs market to roar as school reopenings and wide vaccination usage allows many working parents to get back into the labor force.

“We could see some reversal in August and September’s data because of the delta variant,” Hunter said. “As the delta variant progresses here, if it hampers back-to-school, it could put a dent in.”

Zandi said that some economic indicators — mobility data, restaurant reservations, hours worked, when tracked by private time management systems, consumer and business sentiment — were already sending off warning signals in the South and Midwest in the past month, particularly in states like Florida and Georgia.